Tempo stimato di lettura: 13 minuti

China is leading EV production and consumption

Over the past two decades, China’s automotive sector has achieved notable successes in the transition to the connected, autonomous, shared and electric (CASE) mobility. China has become the world’s leading country in electric vehicle production and consumption since 2015. For the year 2023, about 9.5 million units of new energy vehicles (NEVs) were sold in China, representing over 60% of the world total sales and growing at 38% on a year-to-year basis; among them 7.7 million units were passenger NEVs (CAAM). In comparison, the estimations for passenger EV (BEV+PHEV) sales in Europe and in the North America in 2023 were respectively 3.3 million and 1.6 million units (BNEF, 2023). Besides the quantitative achievements, China is the only country that has so far developed a full value chain of electric vehicle manufacturing, from raw material production, battery making, EV assembly to end-of-life recycling.

The crucial role of industrial policy, and other drivers

The successful deployment of the new EV industry in China is largely the merit of strong and comprehensive industrial policies, covering multiple aspects including raw material management, general emission standards, EV technical requirements, financial subsidies, infrastructure, demonstration zones, etc. There are active policy making both at the central and local governments levels. While the central government provides strategic guidance and funding for fundamental research projects, local governments have more direct roles in policy implementation and adaption, coordinating different actors and stakeholders. There are policies on the demand side, which include in particular purchase subsidies, tax exemptions, practical advantages, charging infrastructure subvention, public fleets, etc.

There are also policies on the supply side, which set increasingly stringent technical requirements for EV manufacturers and battery makers, push OEMs towards electrification through NEV credit system, and promote connected and automated mobility. These multi-level policies have kept evolving with the changing market situations, following the Chinese way of ‘learning from experimentation’. Observations show that the Chinese EV industry policies have gone through several major phases, embodying important changes and evolution, with the goal to not only reinforce China’s leadership in the emerging global EV industry but also accelerate the decarbonisation of its economy. With the Chinese EV industry becoming more competitive and the local EV demand more automatic, the policy focus is shifting on other aspects, such as developing connected and automated mobility, new industrial norms and standards, and a national carbon emission credit trading mechanism.

Other important elements that form a fertile ecosystem for the EV industry in China include:

- Large domestic market size, favourable for local implementation and fast scale-up

- Localised battery supply chain, battery technology maturation, fast growing battery production capacity

- Strong project financing capacity (supported by government, investment funds, banks, stock markets, etc.)

- Increasing vertical integration in EV production (from raw materials to end-of-life reuse and recycling)

- Entrepreneurship (e.g. BYD, Geely, CATL, GEM)

- Close collaboration among different actors (different government agencies, academies, industries, researchers)

- Increasing consumer awareness on the immediate environmental impact of driving EV in cities

- Appealing to new-generation car owners: digitalisation and autonomous driving features.

Chinese EV sales in Europe

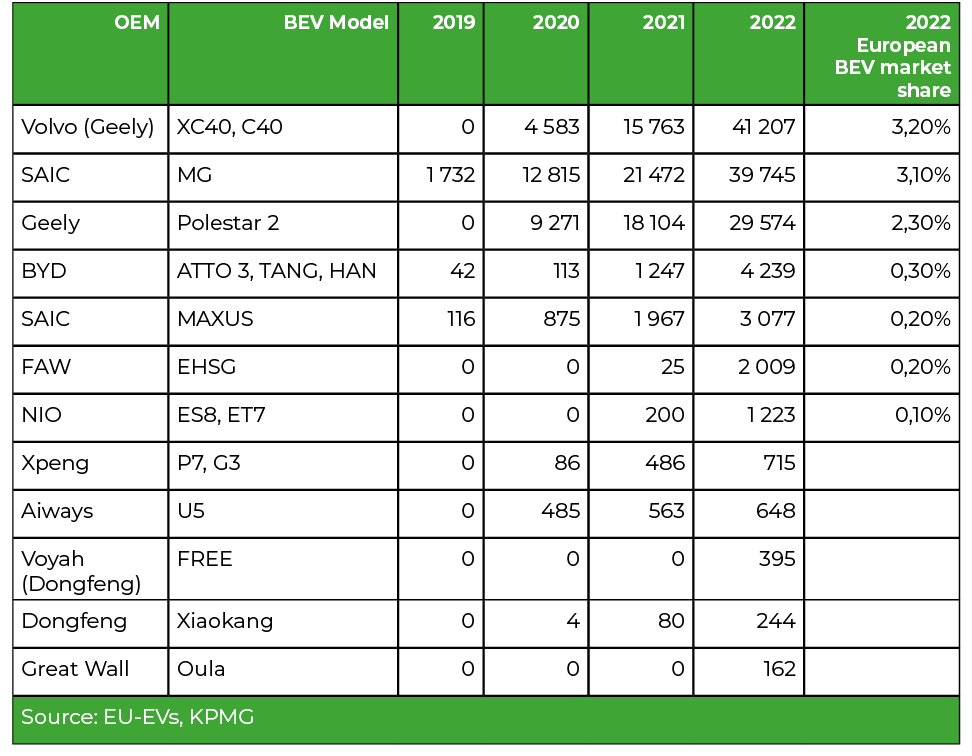

According to statistics from the China Passenger Car Association (CPCA), before 2020, China’s electric car exports to Europe amounted to about 10,000 units; in 2020, the numbers increased to 70,000; in 2021, 48% of Chinese electric cars exported were headed to Europe; in 2022, exports to Europe exceeded 500,000 vehicles, accounting for nearly half of all Chinese electric car exports (KPMG, 2023). Among them, the share of Chinese BEVs (battery electric vehicles) in the European BEV market has increased to around 10%.

Currently, Chinese car manufacturers entering the European market mainly adopt a mixed model of sales, which combines direct sales, agency sales, distribution channels and subscription. NIO opened direct sales stores in Norway and Germany; Xpeng has opened direct sales stores in Sweden; SAIC MG has implemented direct sales networks in 16 European countries, with a total reach of approximately 650 stores. Geely Polestar has agencies in Spain and Xpeng has dealers in the Netherlands and Sweden. BYD has opened more than 140 stores in 15 European countries including Sweden, the United Kingdom, Germany, France, Italy and Spain, and the number of retailers will reach 200 by the end of 2023. BYD has also established cooperation with German car rental company SIXT to supply 100,000 electric cars over the next six years. The subscription model has also been adopted by many Chinese companies.

Lynk & Co has opened 11 experience centers in Europe and users can subscribe to Lynk & Co on a monthly basis. Furthermore, Lynk & Co also uses the B2B mode, where companies or organizations subscribe directly to Lynk & Co Europe on a monthly basis or purchase vehicles directly. Lynk & Co says it has 200,000 monthly subscriptions in Europe as of April 2023 (Reuters, 2023). NIO, based on the opening of directly operated stores, will also provide short-term and long-term subscription services in four European countries: Germany, the Netherlands, Denmark and Sweden.

Chinese EV and battery firms investing in Europe

Driven by the country’s industrial policies, the development of China’s electric battery industry has been a gradual and vertical phenomenon. The initial force was in the middle of the chain, i.e. the processing of raw materials (capital-intensive and polluting); subsequently, the Chinese industry has strengthened at both ends of the supply chain (upstream mineral resources, intermediate battery production technology, and downstream materials recycling), demonstrating a unique dynamism and a strong competitive advantage. The key was the combination of several factors: central and local support policies, enormous investments in resources, strong technological innovations, corporate strategies aimed at strengthening the presence on the chain.

In 2022, the automotive industry accounts for 53% of Chinese investment in Europe, an increase of 33% compared to 2021. This historic growth is mainly due to the fact that Chinese manufacturers of batteries for electric cars are accelerating their “go abroad” (出海) due to domestic overcapacity and declining domestic consumption, and invested directly in creating new production capacities in Europe. For example, CATL and SVOLT (of the Great Wall Motor Group) have set up battery factories in Germany; in particular, the CATL factory has already started mass production at the end of 2022. Other battery companies have also followed their steps. The following table summaries the list of Chinese electric battery companies that have invested in Europe in recent years.

Deepening cooperation between China and Europe

There are many aspects on which Chinese and European firms in the automotive industry could collaborate. A good example is Volkswagen’s investment in one of China’s top 5 battery manufacturers, Gotion Hi-Tech. By becoming Gotion’s largest shareholder in 2021, VW has further secured the supply of batteries for electric vehicle production in China and Europe. Since then, Gotion has made tremendous progress in expanding its business operations. The company announced that it will reach a production capacity of 300 GWh by 2025 and has started mass production of high-nickel cells. The first Gotion battery plant in Göttingen started mass production in September 2023. At the same time, Gotion is establishing a joint venture with Slovakian battery manufacturer Inobat to produce batteries for European electric vehicle manufacturers. The fruitful collaboration between VW and Gotion is based on commercial complementarity and the global trend towards accelerated electrification.

Many other collaborative projects have been started:

- In the production of micro electric vehicles: a good example is the case of the mini EV XEV Yoyo, designed in Italy and produced in China, used for car-sharing.

- In July 2023, Xpeng signed a technology cooperation agreement with VW and received the latter’s investment in exchange for approximately 5% stake.

- In October 2023, Stellantis became a strategic shareholder of Leapmotor with an investment of 1.5 billion euros in exchange for 20% of the company’s capital.

- Down the industrial chain: During the 2023 Davos Summer Forum, CATL said the company was in discussions with a European partner to set up more electric vehicle battery recycling stations in Europe.

- Regarding infrastructure: BYD, Xpeng and NIO have chosen to collaborate with local service providers in Europe to expand charging and trading services and accelerate the construction of charging facilities in Europe.

- Chinese firms have grasped the window opportunity, investing to develop technology leadership and large production capacity, which resulted in vertical specialisation and competitive advantages. The Going Out of the Chinese firms will increasingly challenge host country’s local industrial organisation, pushing for deeper international collaboration, further accelerating the electrification at the global level.